The auto insurance market is changing fast, with two key societal trends driving its evolution. First is the pandemic and the change it has brought to people’s driving patterns. Where before, many office workers used their cars every day to drive to and from their place of work, fewer people now make that same journey every day, due to increased remote and hybrid working schemes. Naturally, they want to see that change in their behavior reflected in the insurance premiums they pay.

The second big trend concerns social justice. It is now accepted that many of the criteria traditionally used by insurers to rate an applicant’s risk – from demographic variables such as income and home location to credit scores and past convictions – can have an unfair impact on certain minority groups within society. Customers now expect insurers to demonstrate fairer policies that are reflective of actual driving behavior and personal usage trends.

Ultimately, policyholders are looking for more control over what they pay, coupled with better personalization of their premiums based on their situation and use cases, resulting in fairer pricing. With the industry now undergoing its most wide-reaching digital transformation in years, the time has come to start evaluating risk more accurately – and to look at the usage of relevant data in doing so, which can also help drive better customer engagement and retention. Among the best and most effective methods to achieve this is mobile telematics.

Telematics driven by the smartphone

Mobile telematics is powerful because of three key characteristics of the smartphone: its ubiquity of usage, the amount of sensor technology already packed into every device and its interactive capabilities. As a result, practically every driver carries a phone capable of reporting on the way they drive – which can ultimately be used to show them how improvements in their behavior can have a positive impact on the premiums they pay.

This last point is critical, because many insurers see mobile telematics simply as a tool for data collection. But when used correctly, it is an amazing tool for boosting the customer experience while improving retention and loyalty, using methodologies that can positively drive behavioral change for the long term. In other words, mobile telematics can make our roads safer and save lives while it improves your book of business at the same time.

If you’d like to get a Mobile Telematics 101 primer before reading this more advanced content, take a look at our overview article.

Now, let’s look at the top five best practices for achieving success with mobile telematics.

1. Reward customers and their behavior will change

You can reinforce good driving behavior with a reward model that will both boost customer engagement and loyalty while improving your insight into individual risk. In essence, your customers will be prepared to improve their driving behavior if they can see that doing so benefits them directly.

As an example of effective reward usage, Carrot Insurance, an IMS client operating in the UK, rewards customers who drive safely via mobile telematics programs named New Driver and Better Driver. Both programs provide customers with continuous access to information on their performance. They have resulted in 56% of customers checking their driving scores daily and 88% of them checking their scores weekly – and this has translated directly into positive behavior change, with a 42% reduction in accident frequency and a 7% reduction in claim severity.¹

Crucially, the investment levels in rewards are not as expensive to the insurer as one may think. Carrot Insurance have calculated that for every 1-2% of premium invested in customer rewards, Combined Operating Ratio drops by 7%.² A very solid return on investment.

2. Implement right-time messaging/coaching

It stands to reason that good driving behavior leads to fewer accidents. In studies conducted by Aite Group among young drivers (who present the highest risks), those receiving regular coaching reinforced by telematics data saw their frequency of accidents drop by an average of between 28% and 49%.³ Moreover, Carrot Insurance also found that guidance, coaching, and frequent feedback through its app increased on-the-road confidence for their drivers.

To inform drivers of what they are doing well and where they need to improve, you need to develop a program of actionable coaching tips and recommendations. It is crucial to deliver the right message at the right time – which is why we like to refer to this concept as right-time messaging. These tips can tell the driver that an unsafe or ill-advised manoeuvre has been detected, in the form of speeding, aggressive acceleration, hard cornering or sudden braking. Carrot Insurance found that, because of right-time messaging and coaching, 56% of their policyholders engaged daily and 88% engaged weekly.⁴ If done well, safer driving and improved driver scores will prevail.

When coupled with a solid rewards program, the power of right-time messaging and coaching is fully realized through positive reinforcement as a key motivator to adjust behavior and improve loyalty.

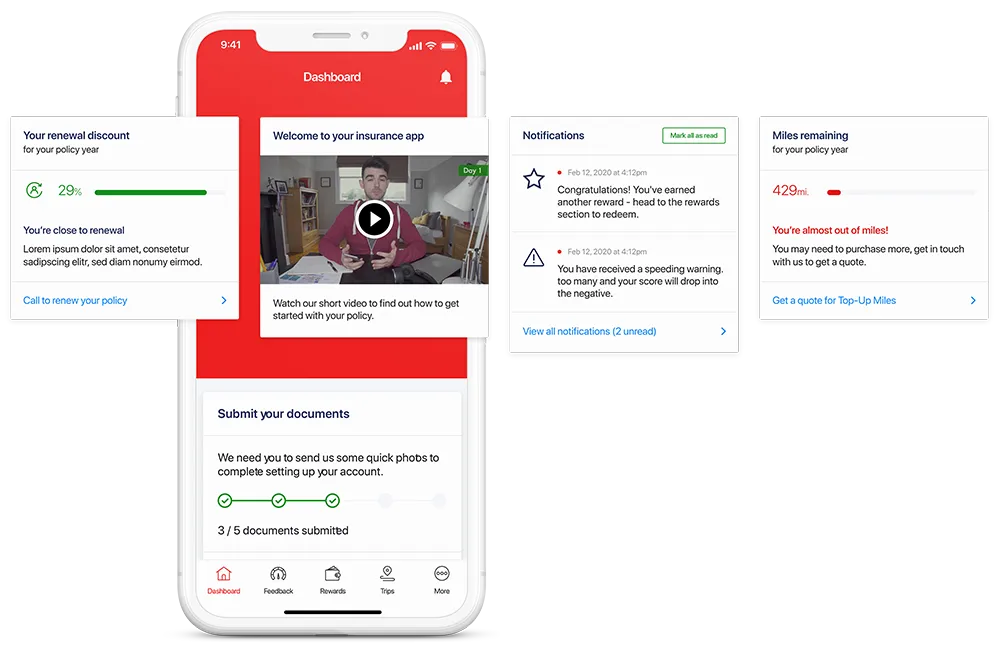

3. Personalize the customer experience

Right-time messaging and coaching to the policyholder is important, but for optimal results, it must be implemented as part of an intuitive customer experience, personalized from end to end. After all, insurance is no longer a one-size-fits-all business. Customers now differ enormously in their needs and a successful program must reflect that. Fortunately, a smartphone application with a flexible underlying architecture can be the perfect platform for personalization.

That underlying architecture is critical, because to achieve better outcomes for you and your customers, you need the capability to deliver a tailored, personalized user experience to every customer – one that evolves with them, over time.

For example, this could begin at the onboarding stage, with video content that supports the customer as they set up the app. It might then offer behavioral coaching content, explaining a rewards program that incentivizes good driving behavior. Real-time feedback and coaching would be delivered during and after daily driving 0 – and specific to their individual driving behavior. In the event of an accident, content would be offered that helps the customer keep themselves safe at the scene, while automatically capturing and transmitting data that could help expedite the claims process. And at every stage, the messaging is personalized to each customer’s journey – never generic.

This may sound like the holy grail, but with the right mobile telematics app framework, it can be achieved quickly and cost-effectively. Time to market is vital, after all. Customer expectations are rising fast, as both disruptive start-ups and established players look to launch personalized experiences of course, mobile app technology is critical in getting this aspect of the customer experience right. It’s therefore important that you review options from technology vendors to uncover those that really offer a highly configurable, dynamic and personalized experience that can truly influence your customers delivering the right type of communication (be it text, audio or video, for example) at the right time.

In a post-pandemic world, where customers expect a more intuitive, seamless experience, the one-size-fits-all insurance model no longer exists. This level of app-driven personalization is vital for any program to succeed.

4.Use the user’s smartphones to identify and stop distracted driving

Industry statistics show time and again that smartphones are often a dangerous distraction when driving. In fact, telematics data reveals that over 50% of driver trips contain at least one distracted driving event⁵. Taking and making calls can divert the driver’s attention from the road, even when undertaken hands-free. Handling of the phone is even worse – after all, a hand on a phone is one less hand on the wheel. Worst of all is looking at the screen which is classed as a high-risk phone distraction and is more common than you might think.

As counterintuitive as it may seem, the solution is to design a mobile telematics experience that decreases mobile phone usage when driving. This can be done by actually incentivizing the user not to use their phone when driving – contrary to common behavior when a phone is present in a vehicle. Done right, you can specifically target distracted driving behaviors, offering the right balance of information (even rewards) for avoiding phone usage while driving.

IMS has helped Canadian insurer Onlia to develop Onlia Sense, a safe driving app that gives drivers scores that reflect how safely they drive. Linked directly to a monthly rewards and cashback program, it enables Onlia to reward its users for adopting safe driving behavior. And it works. Incidents of distracted driving were reduced by 29% overall during the span of a recent program study⁶. Onlia has also seen 70% of Onlia Sense users improve their braking score, 70% improve their cornering and 72% reduce speeding.

You can learn more about how mobile telematics can help improve driver safety at https://ims-2022.bgn.agency/opinion/mobile-telematics-helps-detect-distracted-driving/

5. Plan for future add-ons, such as mobile-based FNOL and claims

Ultimately, mobile telematics data and the programs you build with it can open up strategic opportunities for your business – far beyond your original goals for risk profiling and rating/pricing. Most obviously, these include the addition of new features to the program that can either increase revenues or reduce your costs. Once you have a well-designed app in the hands of your customers, such launches become much easier to deliver. One example is FNOL/crash detection – features than can be added to an existing mobile UBI program or insurance app depending on the telematics solution provider you choose to work with. Benefits for the customer include the ability to be notified immediately when an accident occurs at a time when your policyholder is under the most stress. For you, , it can mean a smoother start to the process, leading to more accurate claim information, a shorter claims shelf life and lower costs. When FNOL notifications are fed through mobile telematics, it can push up to 70% of claims into the digital process, resulting in a significant reduction in claim costs and shelf life. Mobile telematics data can also reduce claim shelf life by up to 30%, allowing your staff to focus on processing the most complex claims.

Mobile Telematics – Providing business benefits you can realize today

All the best practices described above are based on the proper usage of smartphone technology widely available today. From reward programs and right-time messaging that is proven to reduce unsafe and distracted driving, to the potential for mobile telematics to streamline your claims process and customer experience, the effect can be revolutionary – as the results seen by insurers such as Carrot Insurance and Onlia demonstrate. So, while it can be tempting to tout mobile telematics as the future of auto insurance, the reality is better still: there is no need to wait. The benefits are yours to enjoy today with the right usage of this technology.

About IMS

IMS (Insurance & Mobility Solutions) is a vehicle and driving data business, delivering enterprise solutions to global insurers, mobility operators and governments. The IMS DriveSync platform provides the capability for customers to improve their approach to pricing, customer engagement, risk management and claims handling by leveraging telematics data from any source – smartphone apps, aftermarket hardware and OEM embedded units. The company, with offices across the UK, Europe and North America, has analyzed over 15 billion driving miles and its algorithms are fed by trillions of data points each day.

About the IMS Engagement Toolset

The IMS Engagement Toolset is the industry’s most comprehensive suite of engagement tools and techniques. Leveraging telematics data, it is proven to modify driving behavior and generate desired business outcomes, to drive down loss ratios.

It gives you complete control over the ways in which rewards are earned, distributed and fulfilled, offering end-to-end digital interaction. You can deliver messages on a one-to-all, one-to-many or one-to-one basis, including text, images and rich media. By enabling you to set up leagues, leaderboards, achievement milestones and badge systems, it makes a compelling proposition for customers – and it works. 56% of customers receiving the messages check their scores daily, with 88% checking weekly. Overall, they are 39% less likely to have an accident. As a result, a 1-2% premium in investment in rewards will lead to an estimated 7% COB program benefit, with a 1.7% premium will lead to an estimated 3x ROI, through improvements to claims loss ratios.

Learn more about the IMS Engagement Toolset at https://ims-2022.bgn.agency/engagement/

About the IMS One App

The success of any mobile telematics program depends in large part on the customer experience, much of which is necessarily delivered via a smartphone app. With the IMS One App, you can offer a personalized experience tailored to product usage and the customer journey – crucially including their actual driving journeys.

One App is a development framework that makes it quick and easy to create scalable, configurable telematics apps that are proven to work, leading to measurably higher levels of engagement than apps created via other means. One App can help you truly connect with your customers, changing their driving behavior to deliver better outcomes, both for your business and for them.

Learn more about the IMS One App at https://ims-2022.bgn.agency/oneapp/

¹ IMS Carrot Case Study: Capitalizing on a Rewards Program That Really Works for Insurers

² IMS Carrot Case Study: Capitalizing on a Rewards Program That Really Works for Insurers

³ Effective Driver Coaching Partnered with Telematics Improves Auto Claims and Customer Loyalty, Aite Group, February 2020.

⁴ IMS Carrot Case Study: Capitalizing on a Rewards Program That Really Works for Insurers

⁵ IMS Distracted Driving Insights Report: https://ims-2022.bgn.agency/resources/ims-distracted-driving-insights-report/

⁶ IMS Onlia – Telematics Case Study: https://ims-2022.bgn.agency/resources/onlia-sense-telematics-sdk-case-study/