How customer engagement stands at the forefront of a successful UBI proposition.

Telematics-based insurance and UBI programs are now well established around the world. In what is now a highly competitive market, however, success is not guaranteed. To boost brand loyalty, and program ROI, insurers must consider new ways to engage auto insurance customers.

For any insurer, a telematics program represents an essential investment. Yet like any investment, it can still fail to achieve its desired outcomes if it is not managed in the right way. Crucial to the success of these programs is the modification of driver behavior, driven by the necessary levels of policyholder engagement and correct program usage that results in safer driving behavior and increased program ROI. The question many insurers now face is not why seeking better program engagement is needed, but how.

Fortunately, there are proven methods, even tools, to achieve this. In this article, we unpack the top challenges UBI programs face, then look at how the key drivers of engagement can be leveraged to encourage policyholders to drive more safely.

The good news is that there is no need to drop existing programs. The tools we discuss can be used to unlock the full value of any faltering telematics-based UBI program, including those that have just been launched or in market for some time.

The primary challenges facing existing UBI programs

1. Maximizing program ROI

Investing in a UBI proposition can be expensive – and as more insurers introduce UBI programs, features that once delivered a competitive advantage can start to look like mere hygiene factors. While fierce competition is not unique to the insurance industry, the effort required to win new customers is unusually high in this sector. As Independent Insurance Agents of Dallas points out, “the insurance industry has the highest customer acquisition costs of any industry.”¹

It is for this reason that to maximize ROI, insurers must focus on the value delivered by each current customer, throughout the life of their policy. A variety of tools can be used to keep auto insurance customers engaged, without requiring needlessly high investment just before renewal. The tools and methods will be examined shortly.

2. Increasing engagement and policyholder retention

A key driver of ROI is the issue of retaining and engaging auto insurance customers throughout the life of their policies – to ensure perpetual renewal. According to Independent Insurance Agents of Dallas, “the average customer retention rate in the insurance industry is 84% in comparison with a 93% to 95% retention rate maintained by the top five companies in a wide span of industries”.¹ That 10% difference represents a sizeable loss. It stands to reason that if a telematics-driven UBI offering does not offer the right engagement throughout the life of a program, there is a strong chance it will not stand up against a rival that offers a better customer experience.

Crucial to retaining customers, and therefore increasing ROI, is the ability to engage them at the right times, in the right way. Across the industry, many programs are currently failing to do so. Without the right levels of engagement, auto insurance customers can lose interest in even the most sophisticated UBI programs. Failure to engage is proven to come at a cost – that of losing policyholders to competitors and ultimately, poor program ROI resulting in the demise of UBI efforts.

Four ways to engage insurance customers to improve engagement and lifetime retention

We will now reveal the proven methods that can be integrated by usage-based insurers to boost engagement, resulting in improved driving behavior and true program ROI.

1. Right-time coaching and messaging

By identifying the underlying causes of unsafe driving and combining instructional technology with actionable coaching recommendations, accidents and incidents can be greatly reduced. For this method to be effective, coaching and messaging to the user truly needs to be personalized and fed to them at precisely the right time, and with the right content, to really have an impact on behavior.

For example, in studies conducted by Aite Group among young drivers (who present the highest risks), those who underwent regular coaching reinforced by telematics data saw their frequency of accidents drop by an average of 28% to 49%.²

2. Safe driving rewards

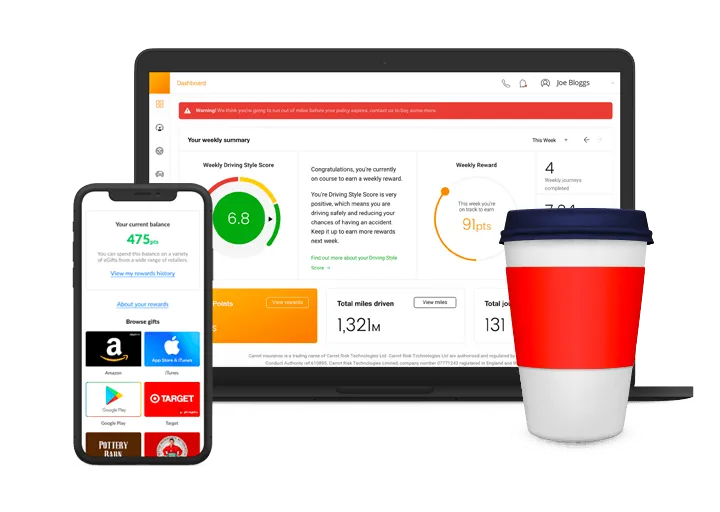

By nature, people like to be rewarded for their efforts – and they respond accordingly. That’s why, as an incentive to drive better, a sequence of rewards can prove particularly effective. Moreover, recognizing the safe-driving achievements of policyholders can increase their brand loyalty. British direct-to-consumer insurer Carrot Insurance rewards customers who drive safely and gives them information regarding their driving behavior to help them do so. The model has resulted in 56% of customers checking their driving scores daily and 88% of them checking their scores weekly.

So what exactly can be used as a reward? The answer is almost anything. Telematics reward systems can include gift cards, reward points systems, event-driven discounts or branded merchandise, for example. Ultimately, it is down to the insurer to tailor them strategically. When implemented correctly, the impact of the rewards will exceed the investment involved. Using Carrot as an example again, analysis has shown that a 1% or 2% investment in rewards and policyholder engagement can yield a 7% cost of revenue (COR) benefit.

3. Gamification

Gamification can be considered another step in improving customer engagement. Rather than solely coaching customers and imploring them to drive safely, it engages the natural will to win or to outdo previous performance. Gamification can be introduced in the form of badges that can be obtained for certain levels of achievement or displaying the performance of top drivers on a leaderboard. These methods have been shown to prove rewarding and motivating to customers. They also make an entire product experience more enjoyable and are best integrated in combination with a system of tangible rewards and coaching techniques.

4. Personalized customer journeys and mobile experiences

Many of the techniques described above are delivered through a smartphone app as the presentation layer – which conveys numerous benefits. The key is ensuring auto insurance customers can access key details relating to their telematics usage-based insurance policy at the right time. For example, when speeding, a driver can be informed in real time that they are over the speed limit and receive tips or videos on how to improve their driving habits – including being dynamically rewarded for improvements.

A truly dynamic smartphone app, built with engagement at the heart, can bring together all the above tools, from timely communication and driving feedback to gamification and safe driving rewards. It thereby represents the ideal vehicle for insurers to differentiate themselves in an extremely competitive market with personalized initiatives that truly motivate driving behavior.

In conclusion

Using the right combination of methods and tools will be the most important step to successfully engaging customers and improving ROI. This is best exemplified by Carrot Insurance, whose combination of coaching, rewarding and gamification has resulted in a 14% loss-ratio improvement for every two points of portfolio score improvement. Ultimately, success relies on rethinking what your customers really need – and devising programs that spark interest and engagement in a fresh real-time, and most importantly motivating, manner.

About IMS

IMS (Insurance & Mobility Solutions) is a vehicle and driving data business, delivering enterprise solutions to over 350 customers including mobility operators, insurers and governments. The IMS Vehicle Data Exchange enables the IMS DriveSync platform to ingest and process data from any source, from OEM embedded units to smartphones and aftermarket hardware. The company, with offices in the UK, Europe and North America, has analyzed more than fifteen billion miles, feeding its algorithms with over a trillion data points.

The IMS Engagement Toolset

The IMS Engagement Toolset is the industry’s most comprehensive suite of engagement tools and techniques. Leveraging telematics data, it is proven to modify driving behavior and generate desired business outcomes, to drive down loss ratio values.

Find out more: https://ims-2022.bgn.agency/engagement/

¹ https://www.iiadallas.org/page/75

² U.S. Auto Insurance: Increase Engagement with Personalized Advice Programs. Insurance Canada. February 2020. https://www.insurance-canada.ca/2020/02/18/aite-group-personalized-advice-programs-increaseengagement/

https://www.insurancebusinessmag.com/us/news/breaking-news/could-insurers-auto-discounts-be-backfiring-220486.aspx